RENTAL MARKETS: OVERVIEW

Rent levels and growth varies substantially around the country depending on the balance of supply and demand, population growth, and infrastructure and job opportunities.

Rents are stable in Brisbane and Adelaide, grew by 1.5% in both Canberra and Melbourne during 2017 with Sydney rents growing by 2.5%*.

"Strong house and apartment price growth in Sydney and Melbourne will force many renters who would like to buy to keep renting. This should support tenant demand for rental properties going forward."

Going forward, rent rises in Canberra will be modest, landlords of older properties in Adelaide and Brisbane will need to become more competitive to attract tenants, as tenants are being attracted to new developments. In Perth and Darwin, further declines in rents are expected to occur due to oversupplies of stock.

INTERSTATE MOVEMENTS (MIGRATION)

Movement of population between the states changes in line with the house price differential and prospects for employment across the states and can affect the prospects for property price rises.

Looking at net interstate migration, there seems to be a shift away from New South Wales. Over the past year, to June 2017 the population changes due to net interstate migration were: -14,859 in New South Wales, +17,182 in Victoria, +17,426 in Queensland, -5,941 in South Australia, -11,722 in Western Australia, +741 in Tasmania, -3,490 in Northern Territory and +663 in Australian Capital Territory.

The outflow of residents from New South Wales has accelerated and is at its highest annual rate since March 2013 while the annual inflow to Victoria is lower than over the previous two quarters.

Queensland now has the greatest annual inflow of residents from interstate of all states and territories and is at its highest level since December 2008. People from other States are being attracted to Queensland because of the improving economy and low property prices.

In South Australia and Western Australia the outflow of residents has slowed moderately while in the northern Territory the outflow is continuing to climb.

The latest available data released in March 2018 now confirms what is happening:

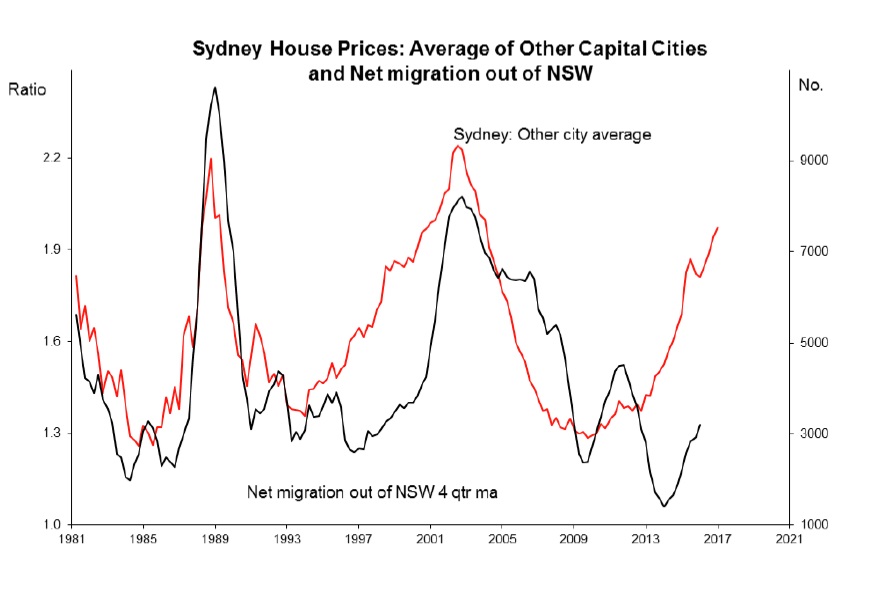

When Sydney house prices become expensive to those in other capitals, the exodus of people from New South Wales always tends to increase.(Have a look at 1988 and 2005!)

This reflects Sydney homeowners cashing in to find better relative value elsewhere.

Based on historic trends, it looks like the Sydneysiders will be soon be arriving in greater numbers in Brisbane. In fact, they already are.

"There are more people leaving NSW for other states and more people travelling to Queensland from other states," Housing Industry Association senior economist Shane Garrett said.

Guess what? Queensland gained 19,000 people last year from the other states in Australia, the highest in a decade and fully 63% of them came from Sydney!

SYDNEY

With completions well ahead of demand, the state’s dwelling shortage lowered to an estimated 39,300 dwellings at June 2017 and is projected to ease to around 12,900 at June 2020. While this will ease owner occupier demand, it will create challenges for investors, who are finding it increasingly difficult to obtain finance

to be able to outbid owner occupiers.

"As a result, house prices are expected to remain stable or decline slightly by a cumulative 4% over the two years to 2018/19 before modest growth returns to take the median house price to $1,150,000 at June 2020, which should be the end of this cycle for Sydney."

With higher interest rates and lower loan-to-value ratios for investor lending, capacity for investors to enter the Sydney market or pay higher prices for apartments is more limited than for houses. This will put downward pressure on apartment prices as investors retreat from Sydney and head to Brisbane especially around 2019-2020. Rental yields in Sydney are also at record lows. The large volume of new apartment construction taking place is likely to push vacancy rates up and put further downward pressure on rental growth as the dwelling deficiency is slowly eroded.

MELBOURNE

The house market is expected to perform well over the next 3 years at least in Melbourne. With Melbourne’s upturn in new supply for apartments being stronger then houses, the market for houses is estimated to still be in undersupply. As a result, median house price growth of 6% is forecast in 2018.

"At June 2020, the Melbourne median house price is forecast to be $940,000, a cumulative 10% increase over the period 2017-2020."

The average apartment price in Melbourne could decline overall due to the number of small, poorly designed apartments drag the value down.

"Although high quality, well designed apartments suitable for first home owners and owner occupiers could maintain their value and increase, especially in the AUD$500- 750,000 price range with the effects of the First Home Buyer incentives taking place.Investors should target this type of property."

BRISBANE

With Sydney and Melbourne having seen strong economic conditions, there has been an increasing number of people migrating to these two cities over recent years, both from elsewhere in Australia and overseas.

With housing affordability now stretched and employment growth accelerating elsewhere in the country it is interesting to see how Queensland in particular is finally starting to see an increase in its share of overseas and interstate migration.

Overall, the outlook for house prices in Brisbane remains good. The local economy will continue its move away from mining and start to recover. Employment prospects should return with huge public sector spending, as well as continuing growth in export sectors such as education and tourism.

Underlying demand is forecast to strengthen and a downturn in new dwelling completions should see the oversupply in the market contained.

"Cumulatively, Brisbane’s median house prices are expected to rise 7% between 2017 and 2020."

Like Melbourne, many poorly designed and overpriced apartments aimed at investors have been constructed, which caused Brisbane’s oversupply. However, good quality apartment projects were valued in 2017 by banks at or near purchase price, and were able to generate full rental occupancy and good yields often exceeding 5%, amongst the highest in the country.

Apartment completions are expected to ease significantly, reducing oversupply.

"By 2020 on current forecasts there will be virtually no new supply appearing in Brisbane apartments."

This could provide the impetus for some strong growth in rentals and prices especially as in 2020 Sydney will reach the end of it's current upward cycle, and investors will be seeking other -cheaper- options with better potential returns.

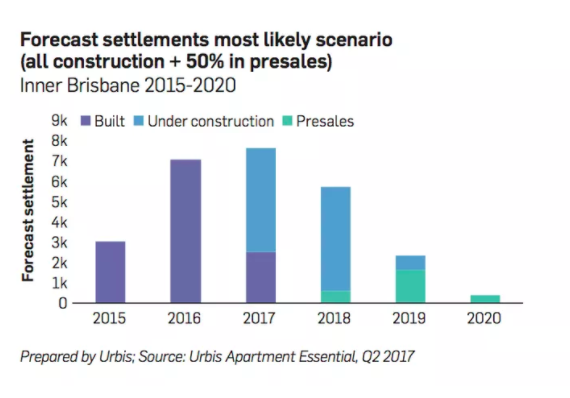

Brisbane saw 3,012 new apartments finish construction in 2015 and 7,064 in 2016 and inner Brisbane peaked in 2017 with around 7,500 apartments. Still far less than the other cities.

Due to a lack of new project launches, future settlements will begin to decrease to 5,691 apartments in 2018, reducing to 2,352 in 2019 and only 396 settlements expected in 2020:

Underlying demand for new apartment stock in Brisbane lies somewhere between 3,000 and 5,000 new apartments per year. The cranes are starting to come down and not being replaced.

By as soon as 2019, the market will be a very different landscape with limited projects under construction and very limited new projects in pre-sales leading to an undersupply. What that means to potential purchasers, is that right now and for the next 12 months or so, it is a particularly good time to buy good quality projects whilst there is some additional supply available, and especially before 1 July 2018 when investors Stamp Duty increases to 7% on that date.

"and especially before 1 July 2018 when investors Stamp Duty increases to 7% on that date."

Overall, Brisbane is at an early stage of its upward cycle, and providing apartment numbers are kept in check, which current indications seem to show, there could be good long term growth anticipated because of low entry prices, population growth and an improving economy. Queensland offer the lowest prices to buy, and lowest taxes of the major East Coast cities.